The Need for Corporate Life Insurance

Life insurance is used for two general purposes in a private corporation – managing risk and creating opportunities. The risk management function is satisfied as life insurance provides the corporation with a tax-free payment in the event of the death of an owner or someone vital to the success of the business. As life insurance also allows for the tax-sheltered build up of cash value additional planning opportunities are additionally created.

The primary needs for corporate owned life insurance to satisfy the risk management purpose are as follows:

Key Person Life Insurance

Any prudent business would insure its company facilities and equipment that is used in creating revenue. It follows then that the business should also insure the lives of the people that run the company and make the decisions which contribute to its profit. Any owner, manager or employee whose death would impair the future growth and success of the company is a key person and should be insured as such.

The proper amount of key person life insurance should be determined through discussion with the company’s management, life insurance advisor and accounting professionals. This discussion would analyze and estimate the amount of the loss that could occur to the company should a key person die.

Funding the Shareholders or Partnership Agreement

When more than one person join together to own a company or partnership, it is common business practice that there be a Shareholder’s or Partnership Agreement. These documents set forth the terms and conditions under which the parties co-exist in the business venture. It also spells out the financial interest that each hold in the concern and how much would be owed to the heirs of a shareholder or partner should that individual die. The use of life insurance owned by the corporation for this purpose guarantees that sufficient funds will be available to trigger the agreement. If there was no life insurance in place and no agreement covering how those funds were to be used, the future existence of the company could be in jeopardy.

To Repay Debt

Like an individual insuring debt to avoid burdening his or her family with outstanding liabilities in the event of death, a business owner should also consider providing life insurance to cover the corporation’s obligations. This would ensure that the net value of the company is optimized when it passes either to the heirs and beneficiaries of the owner or to a successor owner which might be a family member.

One of the advantages of corporate owned life insurance to retire debt is the existence of the Capital Dividend Account. Should the insured business owner die, the life insurance proceeds are received tax-free by the company. The death benefit less the adjusted cost basis of the policy is credited to a notional account – the Capital Dividend Account (CDA). Even if all the life insurance proceeds are paid by the company to the creditors to retire the outstanding debt obligations, the credit remaining in the CDA can still be paid tax-free to the surviving or successor shareholders. This allows any surplus or future earnings to be received by the heirs as tax-free capital dividends up to the amount of the balance of the CDA subsequent to the death of the insured.

To Facilitate Business or Investment Financing

Often when a company borrows to invest or for business operations, the bank will require that the principal(s) of the corporation be insured. In this case, if the life insurance is purchased as a condition of the bank loan being granted, part of the life insurance premiums become tax deductible to the corporation. The reasons for providing life insurance to cover the bank loans are consistent with the reasons stated in repaying debt, but with the bank’s written requirement for life insurance, there is now a tax deduction available as well.

There also may be a situation where an investor would look favourably on the business owner being insured before he or she invests in the company. While there would be no collateral insurance deduction in this case, it may create a comfort level for an investor.

To Assist Family Business Succession

With a family business there is often a desire to transition the ownership of the company to the next generation. One of the common objectives of this transition is to ensure that the company is left financially sound when it is received by the next generation. This can be accomplished by having life insurance on the first generation owner to guarantee that the company is left financially viable and debt-free should the succession occur as a result of the death of the business founder.

The above items are all situations where life insurance is used by a business for risk management purposes. When life insurance is held in a corporation it also can result in attractive planning opportunities. These opportunities include the following:

Estate Planning for the Business Owner

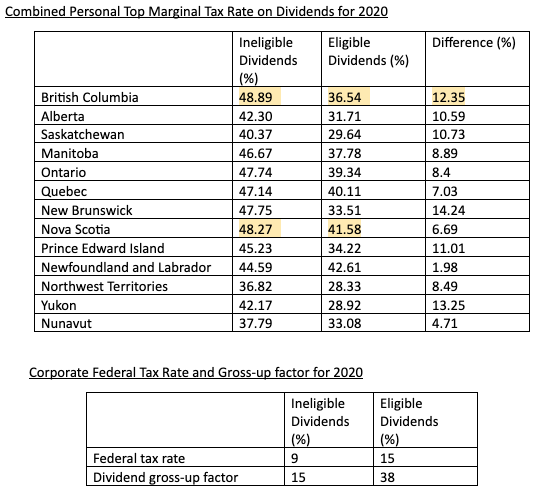

Owners of private corporations in Canada that are qualifying small businesses have the first $500,000 of annual corporate income taxed at a very favourable rate. For example, in B.C. and Alberta it is 12%. The low small business tax rate combined with the Capital Dividend explained above presents the business owner with an opportunity to place life insurance designated for estate planning purposes (e.g. paying taxes arising at death from capital gains), in the corporation.

Sheltering of Corporate Investment Income

While the income tax rate on active business income is quite low, the tax levied against corporate investment income is extremely high. In some provinces, this tax is over 50%. Using tax exempt life insurance policies to shelter this investment income can provide substantial opportunities to defer taxes which would otherwise be payable. All the insurance opportunities for risk management itemized above can also be satisfied by using cash value tax-exempt life insurance. As a result, there are significant planning opportunities available with corporate owned life insurance.

Protecting the Small Business Income Tax Rate

In addition to the above, once a corporation earns more than $50,000 of passive investment income it starts to erode its small business tax limit of $500,000. Once the passive investment income reaches $150,000 it loses all of the small business limit for that tax year. This can be avoided by investing in tax-exempt life insurance policies. Combined with the previous comments not only does the investment grow tax sheltered, it will not impact the small business income limit.

These are the primary reasons why business life insurance is so important. Not only does it help manage risk, it can also provide significant planning opportunities for the business owner. I am available at any time, should you wish to discuss how these ideas could benefit you and your company.